Waterbury, Connecticut… It’s kind of a mix of old factory town vibes and the everyday chaos of traffic. Between 2020 and 2023, almost 19,087 crashes happened here—yep, nearly 36,000 cars and around 45,000 people tangled up in accidents.

A lot of them walked away fine, but still, that’s a crazy amount. Busy roads, old infrastructure, people rushing to work—it adds up. The city’s been putting in safety stuff, sure, but if you drive here daily, you already know: accidents happen.

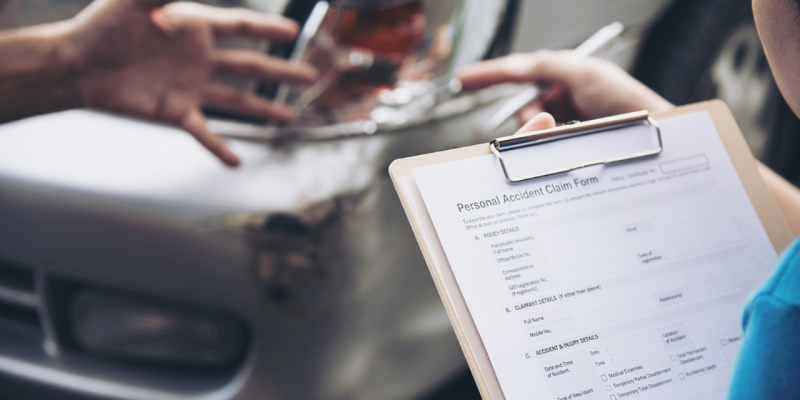

Now imagine this—you get into a crash, file your insurance claim, and then there is a car insurance claim rejection. It stings. But here’s the thing: a denied claim doesn’t mean it’s over.

Insurance companies deny for all sorts of reasons… sometimes legit, sometimes not. Maybe they say it’s excluded, maybe they argue about fault, maybe it’s some missing doc.

Common Reasons Behind Car Insurance Claim Rejection

Car insurance claim rejection is quite common, and it could be because of a policy detail you missed or because of some technical error. If you are aware of the reasons behind this denial, you will be able to avoid these costly mistakes.

- The claim is denied if there is a delay in the claim intimation. You need to read the insurance policy and check the duration your insurer offers.

- Moreover, if you raise a fraud claim, there is a high chance that the insurer will find out and reject the claim.

- If you were drunk while driving, the insurer can reject the claim.

- The insurer also rejects the claim if you were driving with a valid driving license.

- Moreover, the insurer provides you with some terms and conditions. If there is any violation of that, they can reject the claim.

- If the insurance policy has lapsed, they can definitely reject the claim.

- Also, if the damage caused to the car is not included in the policy, they can reject the claim.

- If you have modified the car without informing the insurer, they can reject your insurance claim.

Car Insurance Claim Rejection: Options You Can Try

The point is, you still have options. And if it feels overwhelming, that’s where a Waterbury car accident lawyer can actually step in and guide you.

1. Examining What Led To The Refusal

First off, figure out why. Sounds obvious, but most people just skip to anger without reading. The denial letter? Read it carefully—it usually tells you. Could be missing proof.

It could be that they say you violated the policy. Or just that they’re blaming you. Once you know what excuse they’re leaning on, you’ll know where to poke holes.

2. Gathering And Reviewing Evidence

Next step: stack up your evidence. Photos of the scene, statements from anyone who saw it, the police report. Anything that paints a clearer picture.

Double-check details—dates, signatures, all that boring stuff. If something’s incomplete, they’ll latch onto it. The more solid your pile of proof, the stronger your appeal.

3. Contacting The Insurance Adjuster

Yeah, it means picking up the phone. Talk to the adjuster directly. Keep it calm, even if you want to scream (trust me, I get it). Sometimes it’s just miscommunication, sometimes it’s more.

Ask questions, take notes while you’re on the call. Even little scraps of info can be useful later if you push them further.

4. Filing An Appeal

If the call doesn’t fix things, file an appeal. That’s your chance to shove all the evidence in front of them again, with an explanation of why their “no” doesn’t hold up.

Follow their rules carefully—deadlines, forms, whatever. Appeals get tossed for tiny technicalities, and you don’t want that.

5. Consulting A Legal Professional

Sometimes, honestly, you just need backup. Lawyers deal with this every day. Understanding the role of lawyers can help you a lot. They cut through the jargon and actually explain what your policy says.

And they’re good at pushing back on insurers who try to dodge payouts. It costs money, but in some cases, it’s the only way to get a fair outcome.

6. Exploring Alternative Dispute Resolution

Not every fight has to end in court. You can try alternative dispute resolution. Mediation or arbitration can be faster and less draining. Basically, a neutral third party steps in to help both sides reach something workable. Not always perfect, but it can save time, money, and sanity.

7. Documenting All Communications

This one’s huge: keep track of everything. Emails, letters, even short phone calls—write them down. Date, time, what was said. It might feel like overkill, but if things escalate, that paper trail is gold. It proves what happened and when.

8. Understanding Policy Details

Here’s the part no one likes—actually reading your policy. But you have to. What’s covered? What’s excluded? Sometimes there’s stuff buried in the fine print that helps your case. Knowing the exact wording gives you leverage when you go back to them.

9. Keeping A Calm And Persistent Approach

Dealing with a denial is frustrating; no way around it. But blowing up usually makes things worse. Stay calm, keep pushing. Persistence works better than anger, even if it feels like you’re hitting a wall at first.

10. Seeking Support And Resources

Don’t do it alone. Lean on family, friends, even online forums where people share their own stories. You’ll get tips, encouragement, and maybe even practical advice you hadn’t thought of. Just knowing you’re not the only one helps.

11. Final Steps And Moving Forward

If all else fails? You’ve still got moves. You can file a complaint with Connecticut’s insurance department. Or, if you’re ready for the long haul, talk with a lawyer about going to court. Not easy, not quick, but sometimes worth it. Weigh the pros and cons before deciding.

Be Aware, Avoid Rejection

Car insurance claim rejection sucks, plain and simple. But it’s not the end of the road. Figure out why they said no, gather your evidence, and use the tools available—appeals, mediation, lawyers if needed.

Stay steady. A lot of people have flipped a denial into a payout, and you can too. Also, make sure that you have a valid policy, and you are abiding by the terms and conditions of the policy.